Not sure how these rules apply to you?

Try the GST Decision Assistant to receive a personalised assessment based on your freelance business.

Chapter 1: Two Developers, Two Different Tax Outcomes

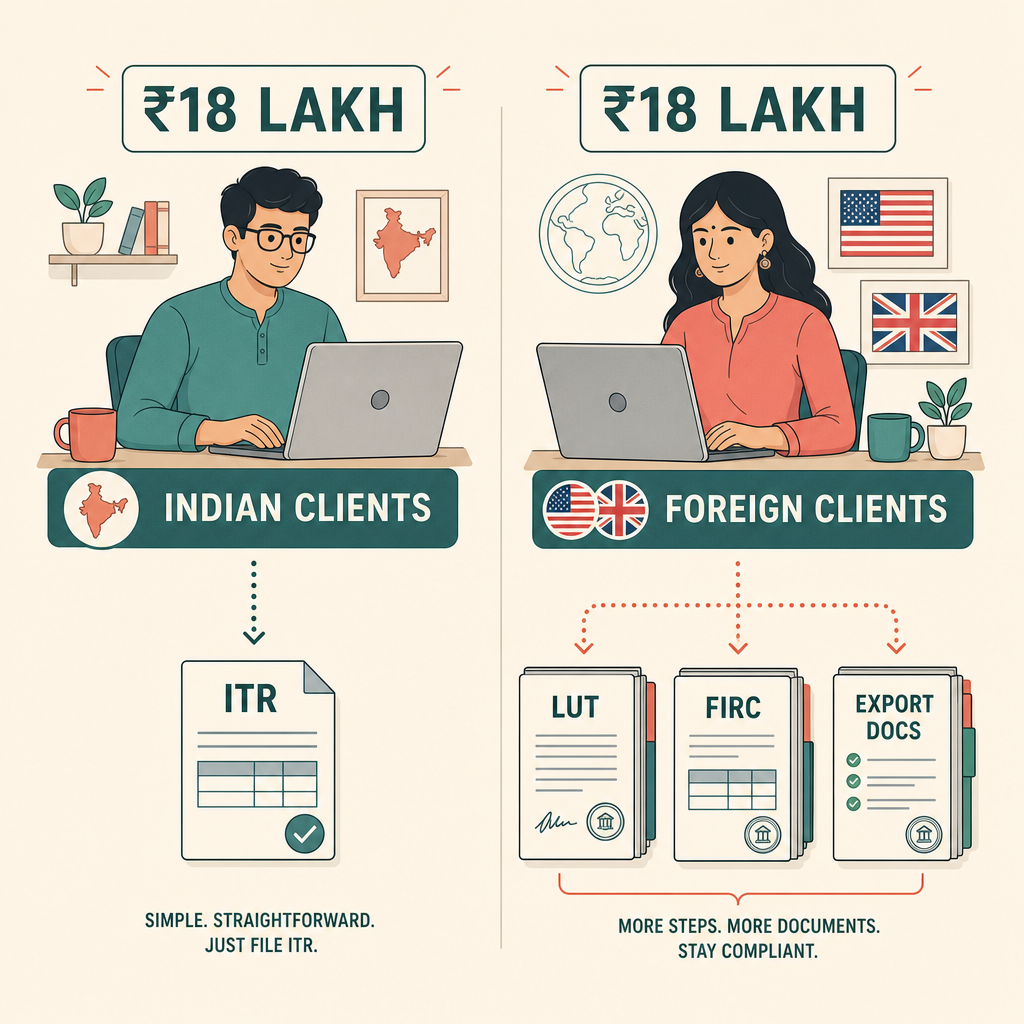

Arjun and Rohan are software developers working as independent freelancers in Pune. They run their operations from their respective home offices, use similar tech stacks, and charge roughly the same hourly rate. At the end of the financial year, they met for coffee and compared their finances.

Both earned exactly ₹18 lakh gross income over the last twelve months.

Arjun exclusively builds mobile applications for local Indian startups based in Mumbai and Bengaluru. Because his income falls under the widely publicized ₹20 lakh GST threshold, Arjun assumes he is exempt from the system. He searches online for "GST registration freelancers," confirms the ₹20 lakh limit, files his standard income tax return, and goes back to writing code.

Rohan assumes the exact same rules apply to him. His client base, however, looks slightly different. Rohan writes backend code for tech companies located in the United States and the United Kingdom.

When Rohan casually mentions his ₹18 lakh income to a tax consultant to verify his income tax filing, the conversation abruptly shifts. Instead of a simple pass, Rohan is asked a series of technical questions. The consultant asks about his Export of Services documentation, checks if he filed a Letter of Undertaking (LUT), asks to see Foreign Inward Remittance Certificates (FIRCs) from his bank, and begins calculating his Aggregate Turnover and verifying Place of Supply.

Two freelancers, living in the same city, working in the same industry, with identical bank balances face completely different regulatory demands.

The discrepancy happens because most independent professionals ask the wrong initial question. Asking *"Do I need GST?"* based solely on total income oversimplifies the system.

To build a resilient freelance business in 2026, you need to understand how the system views your transactions. The relevant questions are different:

- What specific services are you supplying?

- Who are your clients, and where exactly do they reside?

- What other income streams count towards your aggregate turnover?

- Do your specific client interactions qualify as Export of Services under GST?

- What banking documentation will the tax department require to support your tax positions if they review your business three years from now?

This guide breaks down how the GST framework evaluates freelance businesses. Instead of reciting isolated tax laws, we will build a mental model that helps you think about compliance systematically.

Chapter 2: The ₹20 Lakh Limit

Searching for "GST threshold for Indian freelancers" generally brings up a uniform answer: ₹20 lakh. For businesses registered in special category states like Manipur, Mizoram, Nagaland, or Tripura, the limit is often cited as ₹10 lakh.

This number originates from Section 22 of the Central Goods and Services Tax (CGST) Act. The law dictates that a supplier of services must register for GST once their aggregate turnover crosses this specific financial limit in a given financial year.

Because the rule sounds straightforward, freelancers use it as a boundary line. They convince themselves that as long as they stay below this number, the GST ecosystem simply does not apply to them, assuming that staying below ₹20 lakh means zero paperwork and zero tax department scrutiny.

This assumption is incomplete.

The honest framing. Whether GST registration is required depends on the applicable registration provisions, exemptions, and the facts of your business. The ₹20 lakh threshold is only one part of that analysis.

For instance, the Indian government classifies certain services provided to foreign clients as an *Export of Service* — but only when the statutory conditions under GST are satisfied. Such exports are treated as "zero-rated supplies" under GST law, meaning they attract a 0% tax rate. However, to legally claim that 0% rate, you must satisfy specific conditions to demonstrate to the government that the transaction was a legitimate export.

Additionally, the threshold calculation assumes your freelance income is your only financial footprint. The ₹20 lakh limit evaluates financial activity tied to your Permanent Account Number (PAN), governed by the definition of Aggregate Turnover.

✅ Not sure where you stand today? Download the free 5-Minute GST Checklist for Indian Freelancers and review your compliance position in just a few minutes.

Chapter 3: The Bucket Every Freelancer Is Filling

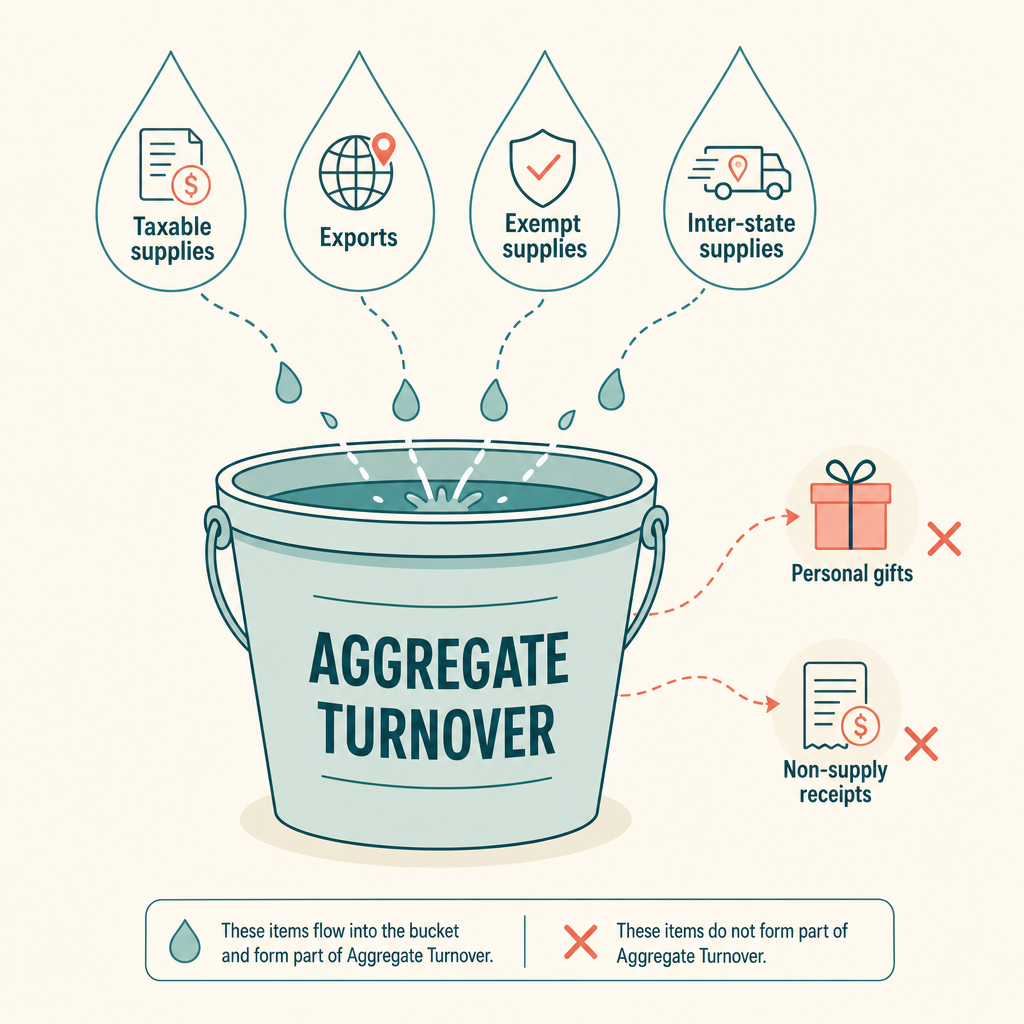

To understand why the threshold calculation surprises many independent professionals, we need to look at the government's terminology. The GST framework does not track "freelance income." It tracks Aggregate Turnover.

Think of your PAN card as a bucket that captures the supplies the GST law includes while determining aggregate turnover. Every time you generate revenue that the law treats as a business supply, a drop goes into that bucket.

The common mistake freelancers make is assuming only their client invoices go into the bucket.

Consider a freelancer who earns ₹15 lakh a year writing copy for Indian ad agencies. Her bucket contains ₹15 lakh.

However, she also owns a small commercial space in her hometown that she rents out for ₹6 lakh a year. Depending on the exact nature of the property and the lease, commercial rental income generally constitutes a taxable supply. That ₹6 lakh goes into the exact same PAN bucket. Her aggregate turnover is now ₹21 lakh.

She has crossed the threshold. She is generally required to register for GST, even though her actual freelance writing income is below ₹20 lakh.

The Aggregate Turnover bucket explicitly captures supplies included by the GST law while determining the calculation, such as:

- Taxable supplies — your standard freelance invoices to domestic clients.

- Exempt supplies — business services you provide that legally do not attract GST.

- Exports — your invoices to overseas clients (even though they may be taxed at 0%, the total value still contributes to turnover).

- Inter-state supplies — services provided to clients in other states under the same PAN.

It is a pan-India calculation. If you have a freelance design gig operating out of Pune and a side-hustle selling digital courses registered in Delhi — both linked to your PAN — they share the same bucket.

It is equally important to know what the bucket does not catch. Receipts that are not considered supplies under GST law — such as a personal monetary gift from a relative — do not contribute to this calculation.

Once your bucket of eligible supplies overflows the applicable limit (₹20 lakh or ₹10 lakh), the standard requirement is to apply for GST registration within 30 days.

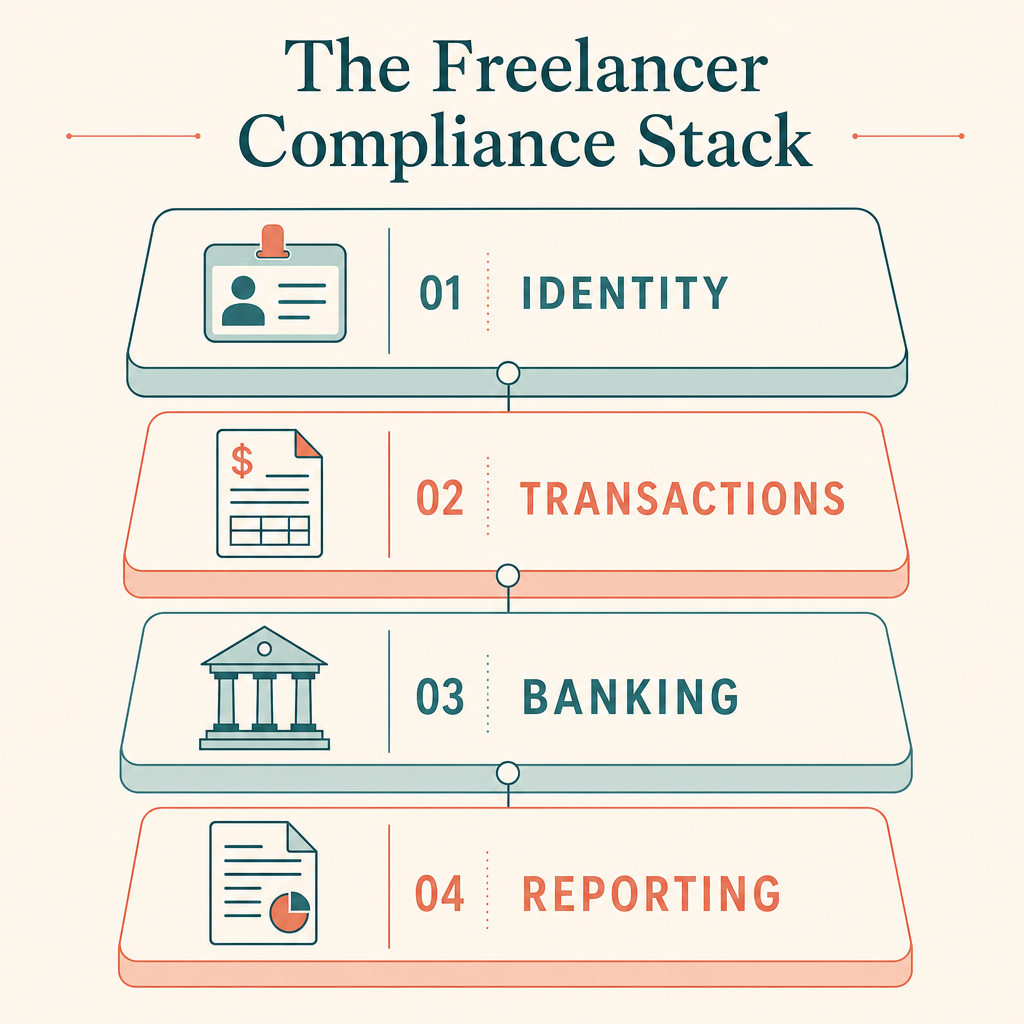

Chapter 4: The Freelancer Compliance Stack

To stop reacting to individual tax rules and start managing your business systematically, you need a framework. At Decompiled.tax, we teach the Freelancer Compliance Stack.

This mental model breaks down your compliance requirements into four distinct layers. Instead of asking "Do I need GST?", you assess the health of each layer in your stack.

Layer 1: The Identity Layer

This is how the government sees your business entity.

- Unregistered: You operate solely on your PAN.

- Registered: You hold a Goods and Services Tax Identification Number (GSTIN).

- Exporter: You hold a GSTIN and an active Letter of Undertaking (LUT) for the current financial year.

Layer 2: The Transaction Layer

This dictates how you interact with your clients commercially.

- Are you issuing standard commercial invoices or GST-compliant tax invoices?

- Are you clearly segregating domestic clients (where applicable GST applies) from international clients (where you state 0% under an LUT)?

- Are your service contracts aligned with the locations listed on your invoices?

Layer 3: The Banking Layer

This covers how money moves from your client to your account.

- Are you receiving domestic bank transfers?

- Are you receiving international wire transfers?

- Are you using payment gateways?

- Are you obtaining the necessary foreign inward remittance documents to help demonstrate that the money originated abroad?

Layer 4: The Reporting Layer

This is how you communicate your financial activity to the government.

- Filing returns like GSTR-1 to report your outbound invoices.

- Filing GSTR-3B to report tax liabilities and input tax credit.

- Filing your annual Income Tax Return (ITR), ensuring the gross receipts match the turnover declared in your GST returns.

When a freelancer faces compliance issues during an audit, it is rarely due to a single isolated error. It usually happens because one layer of their stack failed to communicate with the others. For example, issuing an export invoice at 0% (Layer 2) but failing to secure the required remittance documentation from the bank (Layer 3).

Chapter 5: The Export Challenge

When you work with foreign clients, your compliance stack looks different from a domestic freelancer. You enter the territory of Export of Services under GST.

The government applies a 0% tax rate to qualifying exports of services to encourage foreign currency inflow. However, you do not receive this zero-rating by default. You have to demonstrate that your transaction meets the specific legal conditions of an export.

Imagine sitting across from a tax auditor who points to a ₹1,50,000 credit in your bank account and questions whether it was a domestic transaction subject to 18% tax. How do you support your claim that it was an export?

1. Demonstrating the client's location. An invoice stating a foreign billing address helps. A formal contract or a statement of work further supports the position that the recipient is located outside India.

2. Demonstrating the origin of funds. If your client uses a platform that deposits Indian Rupees directly into your local bank account, the auditor only sees domestic currency. You need to demonstrate that the payment was received in convertible foreign exchange. Freelancers typically do this by presenting a Foreign Inward Remittance Certificate (FIRC) or Electronic Foreign Inward Remittance Advice (e-FIRA) issued by an authorized bank — an important supporting document that helps establish the foreign inward remittance.

3. Navigating the LUT requirement. Registered exporters who wish to export without payment of IGST generally rely on a Letter of Undertaking (LUT). The LUT is filed on the GST portal at the start of the financial year. If an LUT is not available or not filed in time, the compliance consequences become different and may involve paying IGST upfront and claiming a refund later, depending on the facts. That impacts working capital and is worth professional advice.

Chapter 6: Understanding Payment Workflows

Let's look at Layer 3 of the Compliance Stack in detail. How does money actually travel from a foreign client to a freelancer in India, and what documentation is generated?

Depending on how your payment is routed, the documentation available may differ. Before relying on any single document for GST or audit purposes, confirm what your bank or payment provider issues and whether it satisfies your compliance requirements. Platforms change their banking partners regularly, so workflows evolve.

Here are common workflows freelancers encounter:

Direct SWIFT Wire Transfers

When a client wires funds directly from their foreign bank to your Indian bank account, your bank generally handles the foreign exchange conversion directly. In these cases, they typically generate an e-FIRA automatically and report it to the RBI portal.

PayPal

When a client pays via PayPal, the platform receives the foreign currency and routes INR to your local bank through their banking partners in India. Because your local bank only sees an incoming INR transfer from an Indian partner bank, it will not issue an e-FIRA. Freelancers usually have to log into PayPal and download the digital FIRC that PayPal's partner bank issues periodically.

Upwork and Freelance Platforms

Similar to PayPal, platforms like Upwork hold the funds and route withdrawals to your Indian bank through intermediary banking partners. Freelancers often request a specific FIRC from the platform's partner bank or rely on a combination of platform earning certificates and bank statements, depending on the current practices accepted by their assessing officers.

Wise and Deel

Platforms like Wise often use a network of local bank accounts to move money efficiently. Your Indian bank may receive a domestic NEFT/RTGS from a partner account in India, and Wise provides a remittance advice document. However, for strict export compliance, tax officers often look for documentation generated by the Authorised Dealer (AD) bank that processed the foreign exchange into India. Navigating the documentation from modern fintech platforms requires active coordination with your bank and accountant.

📘 Want the complete workflow instead of piecing together information from dozens of blogs? The Indian Freelancer's GST & Income Tax Survival Guide explains GST registration, Export of Services, LUT, FIRC/FIRA, invoicing, documentation systems, and tax filing as one connected system.

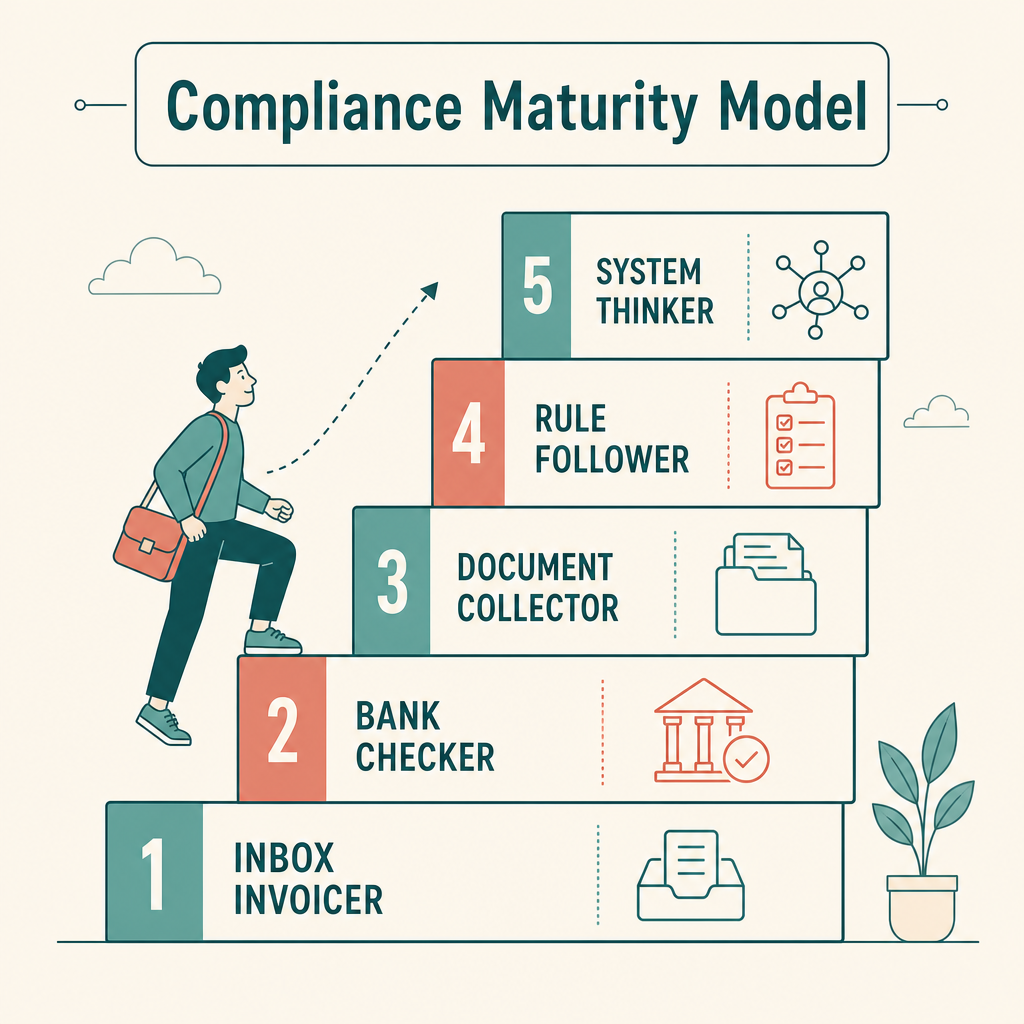

Chapter 7: The Compliance Maturity Model

At Decompiled.tax, we observe how freelancers operate and categorize their administrative habits into the Compliance Maturity Model. Which level describes your current approach?

Level 1: The Inbox Invoicer

You create invoices in a word processor, email them to clients, and wait for the money to arrive. You have no centralized tracker and only consider taxes when the filing deadline approaches. Finding a past invoice requires searching your email sent folder.

Level 2: The Bank Checker

You maintain a basic spreadsheet tracking outstanding payments. You check your bank account to confirm receipts, but you do not systematically map the bank credits to specific invoice numbers. You are aware of your total income but have not evaluated your aggregate turnover.

Level 3: The Document Collector

You are aware of GST and foreign remittance rules. You download remittance documents your bank sends you, and you save your invoices. However, they are stored without a clear organizational system. If an auditor asks you to map a specific bank credit to an invoice from two years ago, it would take significant time to piece the records together.

Level 4: The Rule Follower

You registered for GST because you crossed the threshold or needed it for a client. You hired an accountant to file your returns. However, compliance feels like a stressful administrative burden. You do not fully understand what is being filed, and you operate primarily out of fear of missing deadlines.

Level 5: The System Thinker

You view compliance as an operating system. You use sequential invoice numbering. You download and map banking documentation to invoices monthly. Your LUT is filed on April 1st every year. Because the system runs predictably in the background, you spend minimal mental energy worrying about audits or tax notices.

The goal of evaluating your freelance business is to transition from Level 1 directly to Level 5.

Chapter 8: Common Assumptions and Missteps

As independent professionals build their businesses, they often rely on advice from peers and internet forums. This sometimes leads to adopting absolute rules that lack legal nuance. Here is a look at common assumptions that trap freelancers at the lower levels of the Compliance Maturity Model.

Assumption 1: "I am below ₹20 lakh, so the tax department won't look at me." Running a business strictly based on being "under the limit" leaves you vulnerable to scale. If your income grows and you hit the threshold mid-year, the tax department may review your historical records upon registration. If your invoicing was disorganized or you lacked documentation for foreign payments earlier in the year, establishing a clean audit trail becomes difficult.

Assumption 2: "Foreign clients mean my services are automatically tax-free." This assumption confuses the legal concepts of "exempt" and "zero-rated." An exempt supply means the tax law broadly does not apply. A zero-rated supply means the tax law applies, but the rate is set to 0% — provided you follow the procedural rules and satisfy the statutory conditions for Export of Services.

Assumption 3: "I can organize my bank documents at the end of the year." Compliance is a monthly habit. Attempting to retrieve missing inward remittance certificates from a bank six months after a transaction can be a prolonged administrative task, often requiring you to trace reference numbers through intermediary banks.

Assumption 4: "Registering for GST takes care of everything." Registration is the beginning of the compliance lifecycle, not the end. Once you hold a GSTIN, you enter the reporting layer of the Compliance Stack. Failing to file a "Nil" return during a month with no income can attract statutory late fees and other consequences.

Chapter 9: How to Evaluate Your Position

Rather than relying purely on the ₹20 lakh number, you should evaluate your position based on a combination of your client locations and your PAN-level turnover.

Here is how System Thinkers (Level 5) evaluate their requirements:

| Your situation | What to focus on |

|---|---|

| Below threshold, only Indian clients | Track aggregate turnover monthly. Factor in other PAN-level business income. GST registration is generally not required yet, but sequential invoicing builds good habits. |

| Below threshold, some foreign clients | Monitor turnover closely. Registration may not be immediately mandatory depending on current notifications, but obtaining and storing FIRCs/e-FIRAs for every international payment establishes your export history. |

| Above threshold, only Indian clients | Generally required to register within 30 days. File regular returns and apply the applicable GST rate on domestic invoices. |

| Above threshold, only foreign clients | Register, file an LUT to invoice at 0% without paying IGST upfront, and reconcile bank credits, FIRCs, and export invoices monthly. |

| Above threshold, mixed clients | Run a dual system. Apply GST on domestic invoices and zero-rate (under LUT) on qualifying exports. Keep ledgers cleanly segregated. |

Chapter 10: Building Your Operating System

The ₹20 lakh threshold is a statutory benchmark, but it is not a comprehensive business strategy.

If you build your freelance practice with disorganized invoicing and unmapped bank credits simply because you believe you are "under the limit," you build a fragile structure. When your business scales and you inevitably enter the regulatory system, lacking a historical audit trail creates significant friction.

The core philosophy of Decompiled.tax is that freelancers should understand systems, not just isolated tax laws. We want to help you build the operational machinery that runs your business safely in the background.

The question you ask yourself today should not be: *"Do I need GST?"*

The more productive question is: *"If my freelance business doubles next year, will my current compliance system survive the scale?"*

Build the system before you need it.

The Gritty Details: 20 Real Freelancer FAQs

We gathered common compliance questions from our community of independent professionals. Here is how the principles of the Freelancer Compliance Stack apply to specific scenarios.

1. I crossed ₹20 lakh in February. What exactly do I do now?

Generally, you have 30 days from the day you cross the threshold to apply for GST registration. Once registered, you must begin complying with invoicing and return filing requirements for subsequent transactions. The GST registration guide walks through the process.

2. What if I only have one foreign client and zero Indian clients? Do I still need GST?

If your aggregate turnover crosses the threshold, yes. You are generally required to register, file an LUT, and report the income as a zero-rated export of services, regardless of whether you have domestic clients.

3. Wise gave me a "Remittance Advice" instead of a formal FIRC. Is that okay?

This is a nuanced area. Because fintech platforms often route money through domestic partner accounts, the funds arrive in your account via standard domestic transfers (NEFT/RTGS). While a remittance advice is helpful, tax authorities often prefer documentation generated by the Authorised Dealer (AD) bank that processed the foreign exchange into India. Consult your accountant regarding current accepted practices. See our explainer on FIRC vs FIRA.

4. Is a PayPal FIRC generated automatically?

Not always. While PayPal routes funds through partner banks in India that generate the digital certificates, freelancers usually have to log into their accounts or portals to actively download and save these documents. See FIRC for Freelancers for the retrieval playbook.

5. What happens if I file an LUT late?

An LUT is valid for a specific financial year and is generally required before you make an export supply without payment of IGST. Making export supplies before filing the LUT can complicate your compliance position and may result in IGST being assessed on those prior transactions.

6. My client pays me through Deel. Does that change my export status?

It depends on how Deel is classifying your relationship (Employer of Record vs. Independent Contractor). If you are an independent contractor, you may still be supplying services that qualify as exports under GST. However, the way funds are routed through the platform affects the type of banking documentation you receive, which requires careful reconciliation for GST purposes.

7. My US client wants me to fill out a W-8BEN. Does this affect my Indian GST?

Generally, no. The W-8BEN is a US IRS form used to certify your non-US taxpayer status, which helps your client avoid withholding US taxes on your payment. It is a separate compliance requirement from Indian GST and does not impact your aggregate turnover calculations.

8. Do I need to charge GST on Upwork fees?

No, you do not charge GST on the fees Upwork deducts. Upwork provides a service to you. If Upwork's Indian entity is registered for GST, they will charge you applicable GST on their service fee, which you may be able to claim as Input Tax Credit (ITC) if you are registered.

9. Does Section 44ADA interact with GST rules?

Section 44ADA is a presumptive taxation scheme under the Income Tax Act, separate from the GST Act. However, the gross receipts you declare under Section 44ADA should align with the aggregate turnover declared in your GST returns. Significant mismatches often trigger scrutiny.

10. I work through an Indian agency. Who is my client for GST purposes?

You invoice the entity that contracts and pays you. If an Indian agency hires you and pays you in INR for work that ultimately goes to a US company, your transaction is with the Indian agency. This is generally treated as a domestic transaction subject to standard GST rules.

11. I am an unregistered freelancer. Can I voluntarily register for GST?

Yes, the GST portal allows for voluntary registration. Some freelancers choose this route to claim Input Tax Credit on major business expenses or to meet the vendor requirements of large corporate clients.

12. If I register voluntarily, can I still use the ₹20 lakh exemption?

No. Once you obtain a GSTIN, you are recognized as a registered taxable person. You must comply with all requirements of the GST law, including charging applicable tax and filing returns, regardless of your turnover volume.

13. Can I cancel my GST registration if my income drops below ₹20 lakh next year?

In many cases, yes. If you no longer meet the mandatory registration criteria (and are not maintaining a voluntary registration), you can apply for the cancellation of your GST registration on the portal.

14. What is an SAC code and why do I need it?

SAC stands for Services Accounting Code. It is a classification system used by the tax department to categorize services. You are generally required to mention the correct SAC code for your service category on your tax invoices.

15. What happens if I forget to file a monthly GST return?

Late filing can attract statutory late fees and other consequences. Even a "Nil" return in a month with no business activity is subject to these rules, so registered freelancers should not skip months.

16. I buy software subscriptions from US companies. Does GST apply to me?

Imported software subscriptions and foreign SaaS services can raise Reverse Charge Mechanism (RCM) questions depending on your registration status and the facts of the transaction. We'll cover this in a dedicated future article — talk to your accountant in the meantime if it materially affects your business.

17. Can I use the Composition Scheme to simplify things?

Eligibility for the composition and special composition schemes depends on statutory conditions and should be evaluated carefully — especially where Export of Services or inter-state supplies are involved, since those activities can affect eligibility.

18. How long do I need to keep my FIRCs and invoices?

Under standard GST provisions, registered persons are required to maintain books of accounts and related documents for 72 months (6 years) from the due date of furnishing the annual return for the respective financial year.

19. Does transferring money from Payoneer to my bank count as an export?

Payoneer is a payment facilitator, not the recipient of your services. Whether the transaction qualifies as an export of services rests on the service provided to the foreign client. Payoneer processes the payment and provides documentation (like an e-FIRA through partner banks) that helps demonstrate the funds originated from a foreign source.

20. If I am unregistered, do I still need to keep a sequence of invoice numbers?

Maintaining sequential, professional invoices is a best practice. It establishes a clean historical record for Income Tax purposes — including for those using Section 44ADA or paying advance tax — and creates a reliable audit trail if your business scales and you transition into the GST system.

Continue Learning

- GST Registration for Indian Freelancers — Understand when registration becomes mandatory and how to apply.

- Export of Services Under GST — Learn the five legal conditions that make a transaction a zero-rated export.

- LUT Filing Guide for Freelancers — How to file your annual Letter of Undertaking and invoice foreign clients at 0% IGST.

- FIRC for Freelancers in India — How to collect the right banking documentation for every foreign payment.

- FIRC vs FIRA Explained — The difference between the paper certificate and the digital advice, and which one your bank issues.

- Section 44ADA for Software Developers — How presumptive taxation lets eligible professionals declare 50% of gross receipts as income.

- Advance Tax for Freelancers — The quarterly schedule that keeps you out of Section 234B/C interest penalties.

- GST on Foreign Clients — Why most freelancers don't charge GST to overseas clients, and the conditions behind that rule.

🧭 Need help applying these concepts to your own business? Start with the Survival Guide for the complete system, or book a one-on-one consultation on Topmate if you want to review your specific freelancer setup.