Not sure how these rules apply to you?

Try the GST Decision Assistant to receive a personalised assessment based on your freelance business.

One of the fastest ways to start an argument in a freelancer WhatsApp group is to ask: *"Should I charge GST to my US client?"*

Within minutes you'll hear: *"Yes." "No." "Only if you're GST registered." "Only after ₹20 lakh." "Foreign clients are exempt." "Just file LUT."*

Most of these answers contain a grain of truth. Unfortunately, most are incomplete.

The reason this question causes so much confusion is that freelancers are usually trying to solve three different GST problems at the same time:

- GST Registration

- Export of Services

- LUT Filing

Understanding how these fit together is the difference between confidently issuing an invoice and spending hours decoding contradictory advice.

The short answer

For many Indian freelancers working with genuine foreign clients: no, they do not typically charge 18% GST on export invoices.

But that answer comes with conditions. The correct question isn't *"Is my client foreign?"* — it's *"Does my service qualify as an export of services under GST?"*

That distinction matters. A lot.

Why this topic confuses freelancers

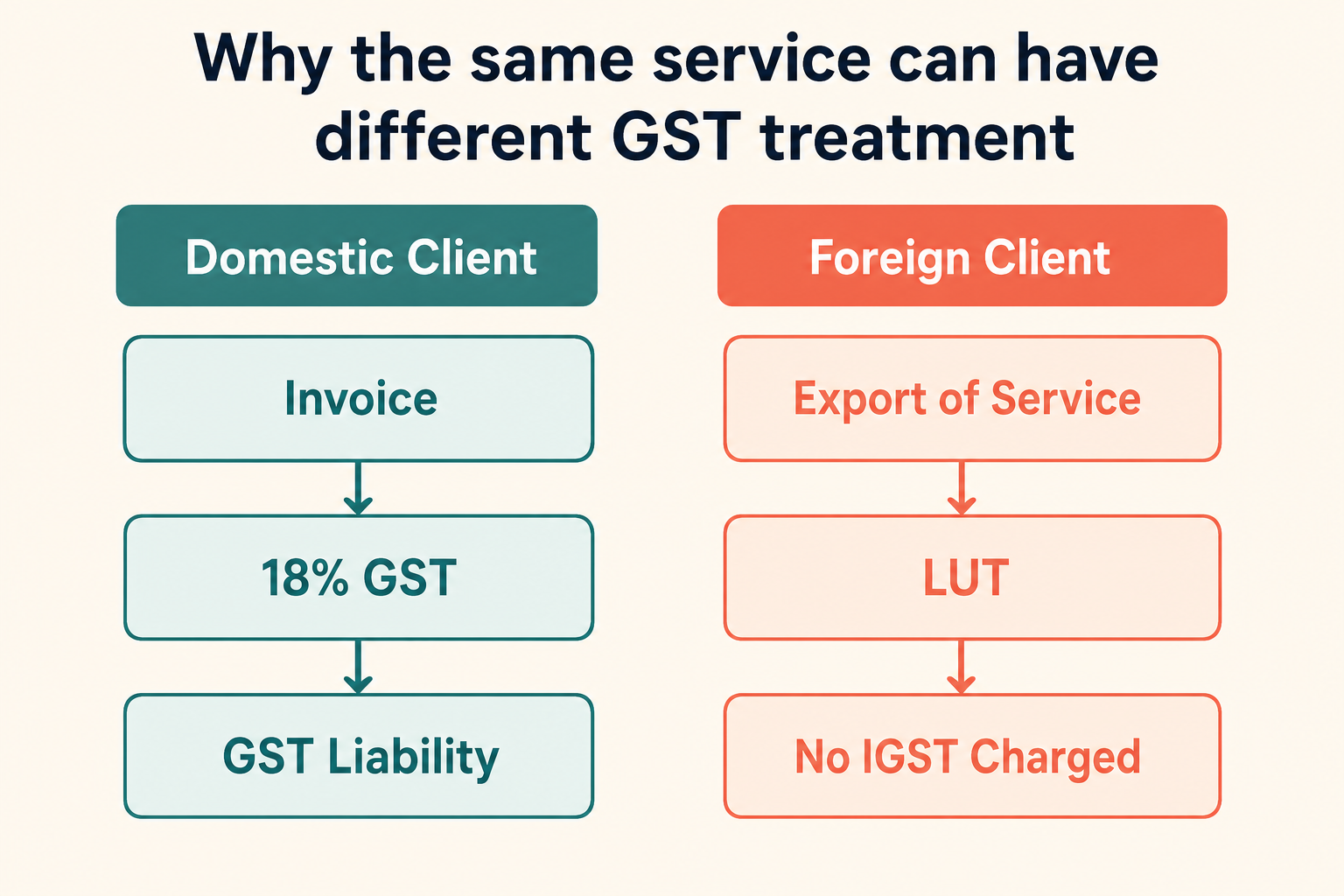

Compare two scenarios.

Scenario A — Client in California, payment in USD, service is ERP consulting → potential export of services.

Scenario B — Client in Mumbai, payment in INR, service is ERP consulting → domestic supply.

Same freelancer. Same service. Completely different GST treatment. The client location changes everything.

Where most blog posts go wrong

Many articles say: *"Exports are zero-rated."* That's true. But it doesn't tell you anything useful.

The question freelancers care about is: *"Can I send an invoice without GST?"* To answer that, we first need to understand what GST considers an export.

What is an export of services?

Under GST, a service is generally treated as an export when specific conditions are satisfied. Among the key considerations:

- Supplier located in India

- Recipient located outside India

- Place of supply outside India

- Payment received in convertible foreign exchange (or as otherwise permitted)

- Supplier and recipient are not merely establishments of the same entity

Miss one of these and the analysis can change. This is why experienced CAs often ask more questions than freelancers expect — they're trying to determine whether the transaction genuinely qualifies as an export.

📘 Foreign-client GST is where most freelancers get it wrong. The Survival Guide breaks down place-of-supply rules, the four export conditions, intermediary edge cases, and exactly when IGST starts applying.

The question most freelancers should actually ask

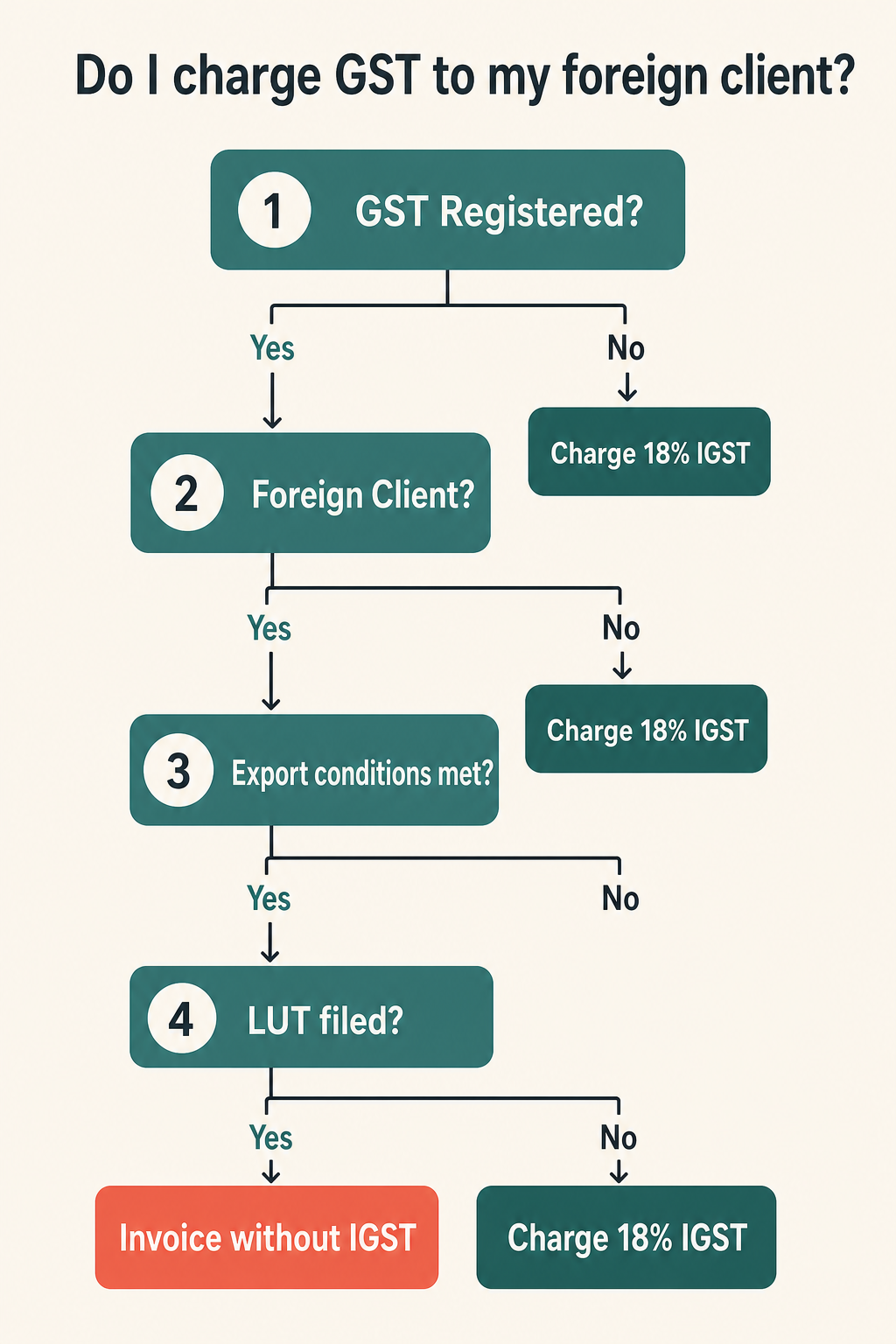

Instead of *"Do I charge GST?"*, ask *"Does this transaction qualify as an export of services?"* If it does, you're in a completely different GST framework.

The role of LUT

This is where many freelancers first hear the term LUT — Letter of Undertaking.

The simplified explanation: an LUT allows eligible exporters to supply services without payment of IGST, subject to applicable conditions. This is why experienced service exporters renew LUT annually. Without LUT, the compliance path becomes more complicated.

Three practical examples

Example 1 — NetSuite consultant in Pune. Client in Texas, ₹32 lakh annual revenue, GST registered, LUT filed, payment in USD via Wise. Assuming export conditions are satisfied, invoices are generally issued without charging IGST.

Example 2 — UI designer in Bangalore. Client in Mumbai, ₹32 lakh annual revenue → domestic supply. GST treatment differs. Same freelancer profile, same income, different GST outcome.

Example 3 — Foreign client, but not an export. This is where many freelancers get surprised. The client may be outside India, yet the transaction may still require deeper analysis depending on the facts. *"Foreign client"* should never be treated as a substitute for a proper export analysis.

The most common mistake

Many freelancers assume: Foreign Client = No GST. That's an oversimplification.

The actual sequence is: Foreign Client → Export Analysis → GST Registration → LUT → Invoice Treatment. Skipping the middle steps is where mistakes happen.

The invoice template most freelancers need

A surprisingly common issue: the GST treatment may be correct, but the invoice may be wrong.

For export invoices, ensure the invoice clearly reflects the nature of the transaction. Many exporters include language similar to:

*"Supply meant for export under Letter of Undertaking without payment of Integrated Tax."*

Your CA may recommend alternative wording based on your situation. The important point: export invoices should not be treated as generic invoices. Required elements typically include client country, currency, GSTIN, export declaration, and a unique invoice number.

What about Wise, Payoneer, and PayPal?

Another source of confusion. Many freelancers believe payment platforms determine GST treatment. They don't.

Whether you receive payment through Wise, Payoneer, PayPal, or direct SWIFT transfer, the export analysis remains fundamentally the same. What changes is the documentation workflow.

Why FIRC and FIRA still matter

Even when GST isn't charged, documentation remains important. For every foreign-client transaction, maintain:

- Invoice

- Client details

- Payment confirmation

- FIRC or FIRA

- Bank statement

- Contract or SOW

Think in systems, not documents. The goal is creating a complete audit trail.

📖 Survival Guide — Chapter 8: Foreign Remittances & Documentation. Wise workflows, FIRC vs FIRA, invoice-to-payment mapping, audit-ready documentation systems.

Edge case: domestic and foreign clients together

Very common. Example: foreign clients ₹18 lakh, domestic clients ₹10 lakh.

Many freelancers incorrectly assume *"I use one GST approach for everything."* In reality, different transactions may require different treatment. Your bookkeeping should clearly distinguish between domestic supplies and export supplies — mixing them creates unnecessary confusion later.

Edge case: foreign client pays in INR

One of the most misunderstood situations. Many freelancers assume Foreign Client = Export. Not necessarily. Payment structure and transaction facts matter. Whenever the payment arrangement deviates from the typical foreign-remittance workflow, review the facts carefully with your tax professional.

Edge case: you forgot to file LUT

This happens more often than people admit. A freelancer gets GST registration, starts exporting, issues invoices, then realizes LUT was never filed.

The appropriate corrective action depends on the circumstances. The lesson: treat LUT renewal as part of your annual compliance process.

📖 Survival Guide — Chapter 5: LUT Filing Workflow. Filing walkthrough, annual renewal process, export invoice templates, common LUT mistakes.

The documentation stack every exporting freelancer should maintain

For each export transaction: invoice, client agreement, payment confirmation, FIRC/FIRA, bank statement, LUT record, email trail.

If you can reconstruct the transaction two years later, your system is working. If not, improve the process.

✅ Want a quick win first? Grab the free 5-minute GST decision checklist — we'll email the PDF and you'll know in five minutes whether GST registration applies to your situation.

Common GST mistakes freelancers make

- Mistake #1 — Assuming foreign clients automatically eliminate GST obligations.

- Mistake #2 — Confusing GST registration with LUT.

- Mistake #3 — Using generic invoice templates.

- Mistake #4 — Ignoring remittance documentation.

- Mistake #5 — Taking GST advice from social media without understanding the underlying facts.

Frequently asked questions

Do I charge 18% GST to a US client? Many qualifying export transactions are invoiced without charging IGST, subject to applicable GST provisions and compliance requirements.

Does GST registration automatically mean I charge GST to foreign clients? Not necessarily. Export treatment is a separate analysis.

Do I need LUT? If you're GST registered and exporting services, LUT often becomes an important part of the compliance framework.

Does Wise change GST treatment? No. Payment platforms do not determine whether a transaction qualifies as an export.

What if I have both Indian and foreign clients? Maintain separate tracking and documentation for domestic and export transactions.

Final thoughts

The biggest GST mistake freelancers make is treating the question as binary. *"Do I charge GST?"* is the wrong starting point.

The better question is: *"Does this transaction qualify as an export of services, and have I followed the correct compliance process?"*

Once you understand the sequence — GST Registration → Export Analysis → LUT → Invoice → Documentation — the answer becomes much clearer. For many freelancers serving genuine foreign clients, the outcome is that export invoices are issued without charging IGST. But the confidence comes not from memorizing the answer; it comes from understanding why.

🧭 Need this dialed in for your situation? Start with the Survival Guide for the full system, or book a 1-on-1 consultation on Topmate if you'd rather walk through your own numbers with someone.

Continue learning

Related guides on Decompiled.tax:

- The ₹20 Lakh GST Myth That Confuses Indian Freelancers

- GST Registration for Indian Freelancers

- LUT Filing for Freelancers

- Export of Services Under GST

- FIRC for Freelancers

- FIRC vs FIRA Explained

- Section 44ADA for Software Developers

For a complete framework covering GST registration, LUT filing, export qualification, foreign remittances, invoicing, and compliance systems, see 📖 The Indian Freelancer's GST & Income Tax Survival Guide.

Want a one-on-one walkthrough of your own situation? Book a consultation on Topmate →