Not sure how these rules apply to you?

Try the GST Decision Assistant to receive a personalised assessment based on your freelance business.

A surprising number of GST mistakes start with a perfectly reasonable assumption:

*"My client is in another country, so this must be an export."*

Sometimes that's true. Sometimes it isn't. And that distinction matters more than most freelancers realize.

Under GST, a service is not considered an export simply because the client happens to be outside India. The transaction must satisfy specific conditions — miss one of them, and the GST treatment can change completely.

That's why experienced CAs ask questions that seem unrelated: *Where is the client located? Where was the service consumed? How was payment received? Is there a contract? Is the recipient actually outside India?* They're trying to determine whether your transaction qualifies as an Export of Services.

Let's walk through how the framework actually works.

Why this matters

Most freelancer GST decisions depend on export status:

- LUT filing — depends on exports

- Zero-rated treatment — depends on exports

- Export documentation — depends on exports

- FIRC / FIRA recordkeeping — often connected to exports

- GST invoicing — often influenced by export treatment

If you misunderstand export classification, you may misunderstand everything downstream.

📘 Want to be sure your invoices actually qualify as exports? The Survival Guide covers all five export conditions in plain English, with sample invoices and the documentation trail that holds up if a notice ever lands.

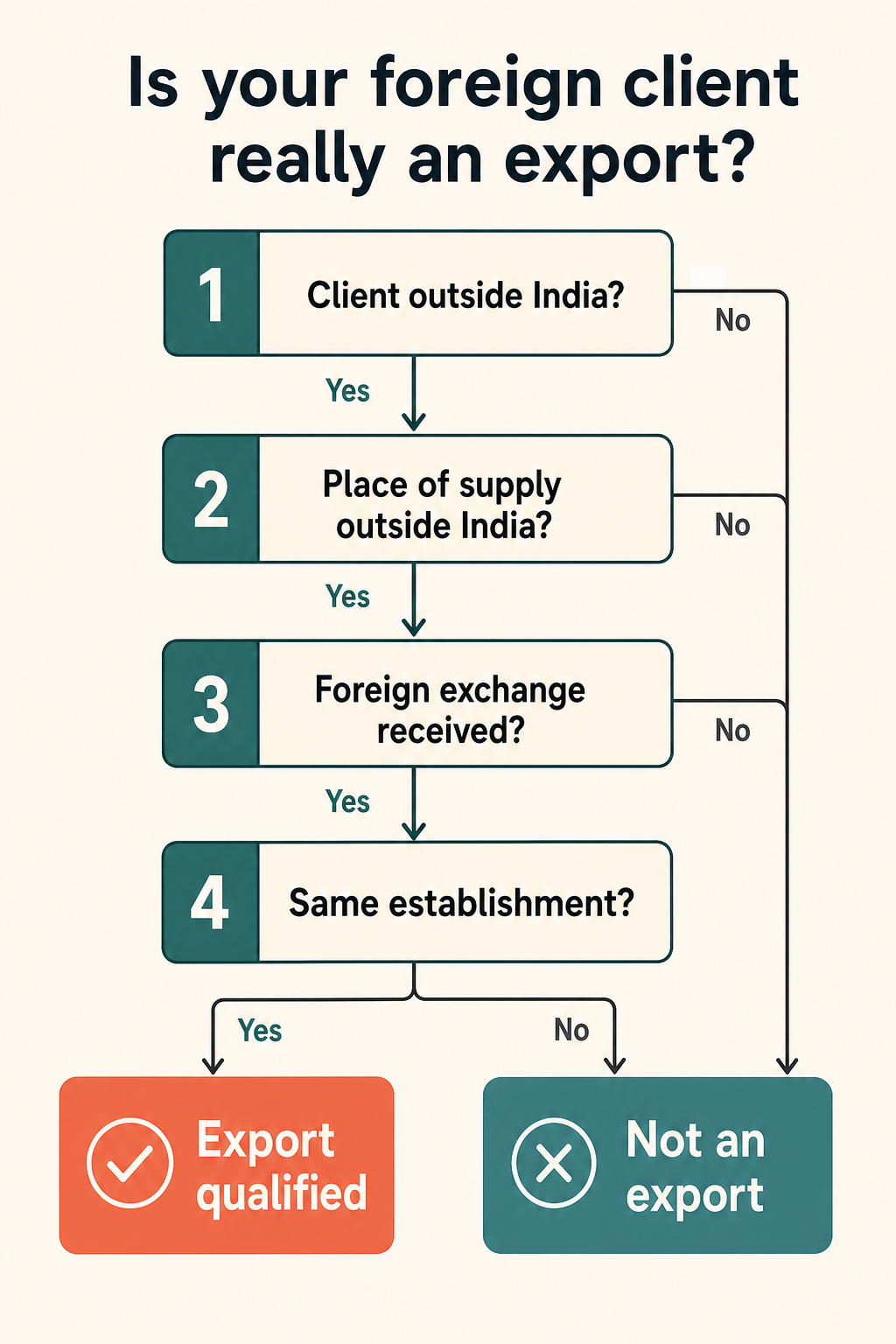

The five conditions

Under GST, a service generally qualifies as an export when all applicable conditions are satisfied. Most freelancers have heard this. Very few understand what each condition means in practice.

Condition 1 — The supplier must be located in India

This is usually the easiest condition to satisfy. A freelancer in Pune, a consultant in Bangalore, a designer in Hyderabad, an ERP contractor in Mumbai — all generally supplying services from India. Most freelancers clear this without difficulty.

Condition 2 — The recipient must be located outside India

This sounds simple. Sometimes it isn't.

Example A — US startup, US address, US management, US contract. Likely straightforward.

Example B — Indian founder, US company, Indian operational team, services consumed primarily in India. Potentially more nuanced.

The lesson: don't focus only on where the invoice is sent. The actual recipient relationship matters.

Condition 3 — The place of supply must be outside India

This is where many freelancers stop reading and call their CA. And honestly, that's understandable. Place of Supply is one of the least intuitive concepts in GST.

A common misunderstanding: *Client outside India = Place of Supply outside India.* Not always.

The correct analysis depends on the nature of the service, the recipient, the delivery model, and the contract structure. For many software developers, consultants, designers, and knowledge workers, the place of supply often ends up outside India. But don't assume — analyze.

Practical example. ERP consultant in Pune, client in Texas, NetSuite implementation → likely export-oriented fact pattern. Same Pune consultant, foreign company client, but training delivered exclusively to an Indian office → different analysis may arise. This is one reason generic GST advice often fails.

Condition 4 — Payment must be received in convertible foreign exchange (or as otherwise permitted)

This condition causes endless confusion. Many freelancers simplify it to *"Client paid in USD. Done."* Not quite.

The compliance question is: can receipt of export proceeds be demonstrated? This is why experienced professionals maintain FIRC, FIRA, bank statements, Wise documentation, and payment confirmations. The issue isn't the currency alone — it's documentation.

📖 Survival Guide — Chapter 8: Foreign Remittances & Documentation. FIRC vs FIRA, Wise workflows, invoice-to-payment mapping, documentation templates. Read the Survival Guide →

Condition 5 — Supplier and recipient must not merely be establishments of the same person

Often ignored because most freelancers never encounter it — until they do. Example: an Indian branch and foreign branch of the same entity. The GST treatment may differ from an independent third-party client relationship. Most solo freelancers won't run into this, but agency owners, international businesses, and complex structures sometimes do.

Why meeting four conditions isn't enough

A common misconception: *"I meet most of the requirements."* Export classification is not a "best effort" test — all relevant conditions must be satisfied. Think of it like a chain. Break one link and the chain stops working.

Real freelancer examples

Let's test the framework.

Example 1 — Software developer in Pune, client in California, USD via Wise, application development. Potentially aligns with a typical export-of-services structure.

Example 2 — UI designer in Bangalore, Indian client, INR payment. Clearly not an export.

Example 3 — Foreign client, Indian operations, service consumed primarily in India. Requires deeper analysis. This is where generic internet advice becomes dangerous.

Why export status changes your GST workflow

Once a transaction qualifies as an export, other pieces begin to matter: GST Registration → LUT → Export Invoice → FIRC/FIRA → GST Returns. This is why export classification sits at the center of freelancer GST compliance.

📖 Survival Guide chapters: Chapter 4 — GST Registration for Freelancers · Chapter 5 — LUT Filing Workflow · Chapter 7 — Export of Services Explained. Together these walk through the complete export compliance process.

✅ Want a quick win first? Grab the free 5-minute GST decision checklist — we'll email the PDF and you'll know in five minutes whether GST registration applies to your situation.

Common export mistakes freelancers make

- Mistake #1 — Assuming foreign client automatically means export.

- Mistake #2 — Ignoring place-of-supply analysis.

- Mistake #3 — Maintaining weak payment documentation.

- Mistake #4 — Confusing LUT with export status. *LUT does not create exports — it operates within an export framework.*

- Mistake #5 — Treating invoices as the only evidence required.

The export readiness checklist

Before treating a transaction as an export:

- ✓ Client outside India?

- ✓ Supplier located in India?

- ✓ Place of supply analyzed?

- ✓ Payment documentation available?

- ✓ FIRC/FIRA maintained?

- ✓ Contract retained?

- ✓ LUT filed (if applicable)?

If any answer is unclear, investigate before assuming export treatment.

Frequently asked questions

Is every foreign client automatically an export? No. The transaction must satisfy the applicable export conditions.

Does Wise affect export classification? No. Payment platforms do not determine export status.

Do I need FIRC or FIRA? Strong documentation is generally considered good practice when receiving foreign payments.

Does LUT create export status? No. LUT is a compliance mechanism used after export qualification is determined.

What if I have both domestic and foreign clients? Each transaction should be analyzed separately.

Final thoughts

The biggest GST mistake freelancers make is treating exports as a geography question. It isn't — it's a classification question. The client being outside India is only one piece of the puzzle. The real question is whether the transaction satisfies the export framework as a whole.

Once you understand the five conditions, many other GST questions become easier:

- Do I charge GST?

- Do I need LUT?

- Why does my CA want FIRA?

- Why am I maintaining export documentation?

They're all downstream of the same decision. And that's why understanding export of services is one of the most valuable things an Indian freelancer can learn.

🧭 Need this dialed in for your situation? Start with the Survival Guide for the full system, or book a 1-on-1 consultation on Topmate if you'd rather walk through your own numbers with someone.

Continue learning

Related guides on Decompiled.tax:

- The ₹20 Lakh GST Myth That Confuses Indian Freelancers

- GST Registration for Indian Freelancers

- LUT Filing for Freelancers

- Do Indian Freelancers Charge GST to Foreign Clients?

- FIRC for Freelancers

- FIRC vs FIRA Explained

For a complete framework covering export classification, GST registration, LUT filing, invoicing, remittance documentation, and freelancer tax planning, see 📖 The Indian Freelancer's GST & Income Tax Survival Guide.

For the complete workflow — from onboarding a foreign client to filing your ITR — see the Getting Paid by Foreign Clients hub.

Want a one-on-one walkthrough of your own situation? Book a consultation on Topmate →