Every freelancer eventually hears a version of this claim:

"Under 44ADA, you only pay tax on half your income."

Sometimes it's presented as a tax hack. Sometimes as a loophole. Sometimes as something every software developer should automatically use.

None of those explanations are particularly helpful.

The reality is more interesting. For some software developers, Section 44ADA can significantly simplify tax compliance while reducing the amount of income subject to tax. For others, applying it without understanding the rules can create unnecessary risk.

This guide explains how Section 44ADA actually works, where software developers fit into the picture, what grey areas exist, and how experienced freelancers evaluate whether it makes sense for their business.

The question most developers are really asking

Let's start with a simple example.

Arjun is an independent NetSuite consultant.

- Annual receipts: ₹40 lakh

- Business expenses: Internet, laptop, software subscriptions, co-working space

A friend tells him: *"Use 44ADA. Only 50% gets taxed."*

Arjun's immediate question isn't *"What is Section 44ADA?"*. It's *"Am I actually eligible?"*

That's the right question.

What Section 44ADA was designed to do

Historically, professionals often had to maintain detailed books of account, expense records, supporting documentation, and compliance records. For many independent professionals, this created a disproportionate compliance burden.

Section 44ADA introduced a presumptive taxation scheme for specified professions. Instead of proving every expense, eligible professionals may declare a prescribed percentage of gross receipts as income.

The commonly discussed figure is 50%.

In simple terms: if gross receipts are ₹40 lakh, income may be declared at ₹20 lakh. The remaining amount is presumed to represent expenses and business costs.

This is why the provision attracts so much attention.

The first important nuance

44ADA does not say *every freelancer can automatically claim 50%*. Eligibility matters.

This is where internet advice becomes dangerous. Many discussions skip directly to tax savings and ignore qualification.

The correct starting question is: Does my profession fall within the scope of Section 44ADA?

Where software developers enter the picture

This is one of the most debated topics in Indian freelancer tax circles.

Unlike doctors, lawyers, architects, and chartered accountants, software developers are not explicitly named in the traditional list of professions most people associate with 44ADA. However, many technology professionals have relied on the category of "Technical Consultancy".

This is where interpretation becomes important. Different professionals may take different views depending on the nature of services being provided.

- ERP Consultant — designing solutions, advising clients, implementing systems, providing technical expertise. Often easier to position as technical consultancy.

- Independent Developer — writing code full-time for a single client. Potentially more nuanced.

- Fractional CTO — architecture guidance, technical leadership, strategic advisory. Often closer to consultancy in substance.

Eligibility should be evaluated based on the facts of your engagement rather than a simplistic label.

📘 Trying to decide if 44ADA actually fits your business? Chapter 10 of The Survival Guide has the eligibility worksheet, lock-in trap examples, and an old-vs-new regime comparison for foreign-client developers.

Why your contract matters more than most people realize

Many freelancers focus on invoices. Experienced professionals also review contracts.

Consider two examples.

Example A — Role: *Senior Software Engineer*. Responsibilities: daily development, sprint participation, coding tasks.

Example B — Role: *Technical Consultant*. Responsibilities: solution architecture, ERP advisory, technical design, system recommendations.

Both individuals may write code. But the commercial nature of the engagement differs. When discussing 44ADA, substance matters.

The biggest mistake developers make

They assume: *Revenue received through Wise = consultancy.*

The payment method is irrelevant. What matters is:

- Nature of services

- Engagement structure

- Supporting documentation

- Consistency of treatment

What counts toward gross receipts?

This question rarely receives enough attention. Developers often ask:

- Do reimbursements count?

- What about pass-through costs?

- What about exchange-rate gains?

These should be evaluated carefully with your tax professional because the treatment depends on the facts. The important lesson: don't blindly use gross receipts from a dashboard and assume the calculation is complete.

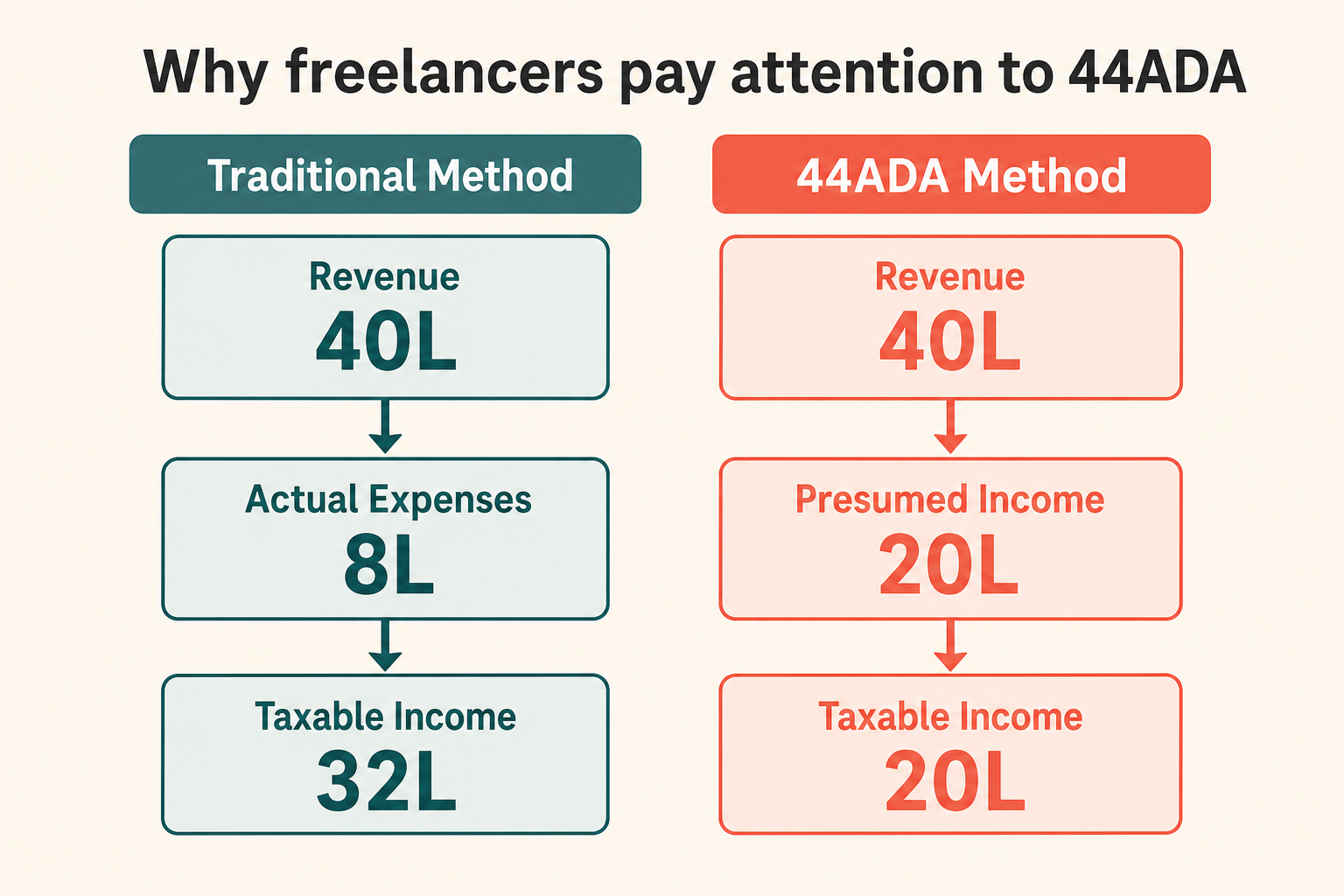

Practical example: NetSuite consultant

A realistic scenario.

Revenue: ₹48 lakh

Expenses: Travel ₹2L, Software ₹1L, Internet ₹60,000, Hardware ₹1L — actual expenses ₹4.6 lakh.

Without 44ADA: ₹48L − ₹4.6L = ₹43.4L taxable.

Using presumptive taxation: ₹48L × 50% = ₹24L presumed income.

This illustrates why many consultants evaluate 44ADA seriously.

The question nobody asks

What if your actual expenses exceed 50%? This happens more often than people think — hiring subcontractors, large travel expenses, significant software costs, hardware-intensive work.

In those situations, 44ADA may not always produce the best outcome. The assumption that 44ADA is always superior is incorrect. The right choice depends on economics, not internet folklore.

What about GST?

A common misconception: *"I'm using 44ADA, so GST doesn't matter."*

These are entirely different frameworks. 44ADA is income tax. GST is indirect tax.

A freelancer may use 44ADA, hold GST registration, file an LUT, and maintain FIRC/FIRA records — all at the same time.

📖 Survival Guide references: Chapter 4 — GST Registration for Freelancers · Chapter 5 — LUT Filing Workflow · Chapter 8 — Foreign Remittances & Documentation.

Documentation still matters

Another common misunderstanding: *"44ADA means no records."* Not true.

While compliance requirements may be simplified, maintaining documentation remains good practice. For every foreign client, keep your contract, invoice, payment records, FIRC/FIRA, and bank statements. Future-you will be grateful.

Edge case: one large client

One client. One contract. Most income from a single source.

This doesn't automatically disqualify someone from 44ADA. But it is worth examining the broader nature of the relationship:

- Are you operating independently?

- Are you providing professional services?

- Is the engagement consultancy-oriented?

Edge case: developer + agency owner

Many freelancers evolve into agencies. Revenue sources may include consulting, development, subcontracting, managed services. At that point, the analysis becomes more complex — the answer may not be identical to that of a solo consultant.

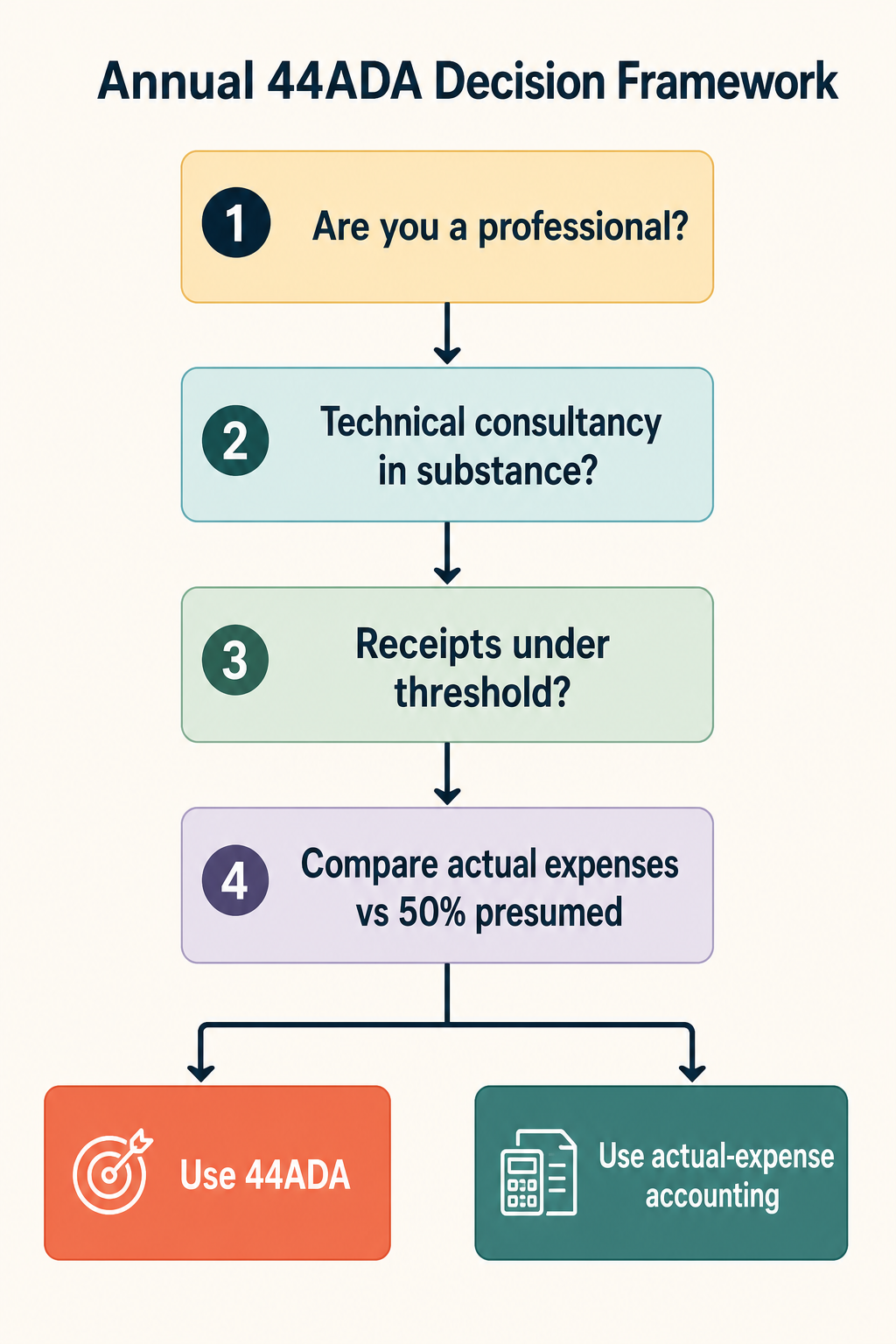

The annual 44ADA review

Every year, ask:

- What services did I actually provide?

- How are those services described in contracts?

- What were my gross receipts?

- Would actual-expense accounting produce a better outcome?

- Is my tax treatment consistent with the facts?

✅ Want a quick win first? Grab the free 5-minute GST decision checklist — we'll email the PDF and you'll know in five minutes whether GST registration applies to your situation.

Common 44ADA mistakes

- Mistake #1 — Assuming every software developer automatically qualifies.

- Mistake #2 — Copying someone else's tax strategy.

- Mistake #3 — Ignoring contract language.

- Mistake #4 — Confusing GST with income tax.

- Mistake #5 — Never evaluating actual-expense accounting.

Frequently asked questions

Can software developers use Section 44ADA? The answer depends on the nature of the services and how they align with the applicable professional categories.

Is 44ADA a tax loophole? No. It is a statutory presumptive taxation provision.

Do I need GST if I use 44ADA? These are separate issues.

Does Wise affect 44ADA eligibility? No. Payment platforms do not determine eligibility.

Is 44ADA always better? No. The economics of your business matter.

Final thoughts

The biggest misconception about Section 44ADA is that it's about saving tax. It isn't. It's about choosing the tax framework that best reflects the reality of your professional practice.

For some software developers, consultants, ERP specialists, and technical advisors, 44ADA can be a remarkably efficient way to simplify compliance. For others, actual-expense accounting may be more appropriate.

The right answer is rarely found in a viral LinkedIn post. It's found by understanding your services, your contracts, your revenue model, and your documentation.

The goal isn't to force yourself into 44ADA. The goal is to determine whether your business genuinely fits it.

🧭 Need this dialed in for your situation? Start with the Survival Guide for the full system, or book a 1-on-1 consultation on Topmate if you'd rather walk through your own numbers with someone.

Continue learning

Related guides on Decompiled.tax:

- The ₹20 Lakh GST Myth That Confuses Indian Freelancers

- GST Registration for Indian Freelancers

- LUT Filing for Freelancers

- FIRC for Freelancers

- FIRC vs FIRA Explained

- Advance Tax for Freelancers

For a complete freelancer-focused framework covering 44ADA, GST, LUT, foreign remittances, invoicing, and tax planning, see 📖 The Indian Freelancer's GST & Income Tax Survival Guide.

Want a one-on-one walkthrough of your own situation? Book a consultation on Topmate →