Not sure how these rules apply to you?

Try the GST Decision Assistant to receive a personalised assessment based on your freelance business.

If you've spent any time in freelancer communities, you've probably seen advice like:

*"You need GST as soon as you get a foreign client."*

A few comments later:

*"No, GST isn't required until ₹20 lakh."*

Then someone else says:

*"Just get GST registration and file LUT."*

At this point, most freelancers are more confused than when they started.

The reality is that GST registration is one of the most misunderstood topics in Indian freelancing. Not because the law is impossible to understand — but because most articles explain GST. They don't explain how freelancers actually make decisions.

This guide takes a different approach. By the end, you'll understand when GST registration becomes relevant, why foreign clients complicate the discussion, how exports fit into the picture, the common mistakes freelancers make, and a simple decision framework you can use before talking to your CA.

The 60-second answer

Many freelancers focus on one question:

*"Do I have foreign clients?"*

The GST system usually starts with a different question:

*"What is your aggregate turnover?"*

That's why two freelancers with identical clients can end up with very different compliance obligations. The answer often depends on revenue levels, the nature of services, export classification, and the specific GST provisions that apply to your situation.

If you're looking for a simple yes/no rule, you're going to be disappointed. If you're looking for a practical framework, keep reading.

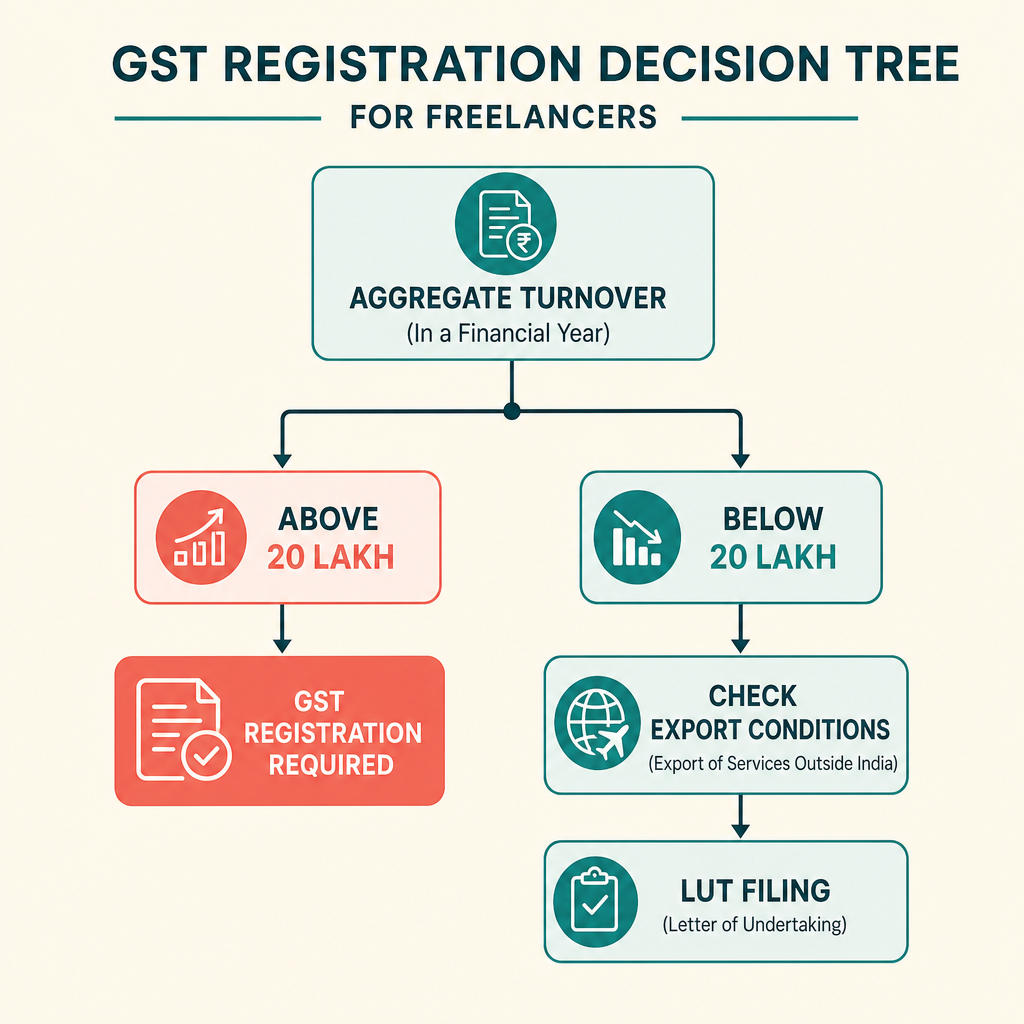

The GST registration decision tree

This is the framework I wish more freelancers saw. Instead of memorizing rules, walk through the questions.

Question 1. Do you provide services as a freelancer, consultant, contractor, creator, agency, or independent professional? If yes, continue.

Question 2. What is your aggregate turnover? Below the applicable threshold → continue analysis. Above the applicable threshold → GST registration generally becomes relevant.

Question 3. Are your clients domestic, foreign, or both? The answer influences what comes next.

Question 4. Do your foreign transactions qualify as exports of services? This is where many freelancers make incorrect assumptions. *A foreign client does not automatically mean export.*

Question 5. If registered, do you need LUT for exports? Different question. Different answer. Different compliance process.

Why most freelancers get confused

Because three separate topics are constantly mixed together:

- GST Registration — Do you need a GST number?

- Export of Services — Do your foreign transactions qualify as exports?

- LUT — Can you export without charging IGST?

These topics are connected. They are *not* interchangeable. One of the most common mistakes freelancers make is assuming: *"I understand exports, therefore I understand GST registration."* Not necessarily.

A real example

Consider two freelancers.

- Freelancer A — Software developer, revenue ₹12 lakh, US clients only.

- Freelancer B — Software developer, revenue ₹28 lakh, US clients only.

Same profession. Same country. Same payment platform. Different compliance situation. The difference isn't the client — it's the overall facts.

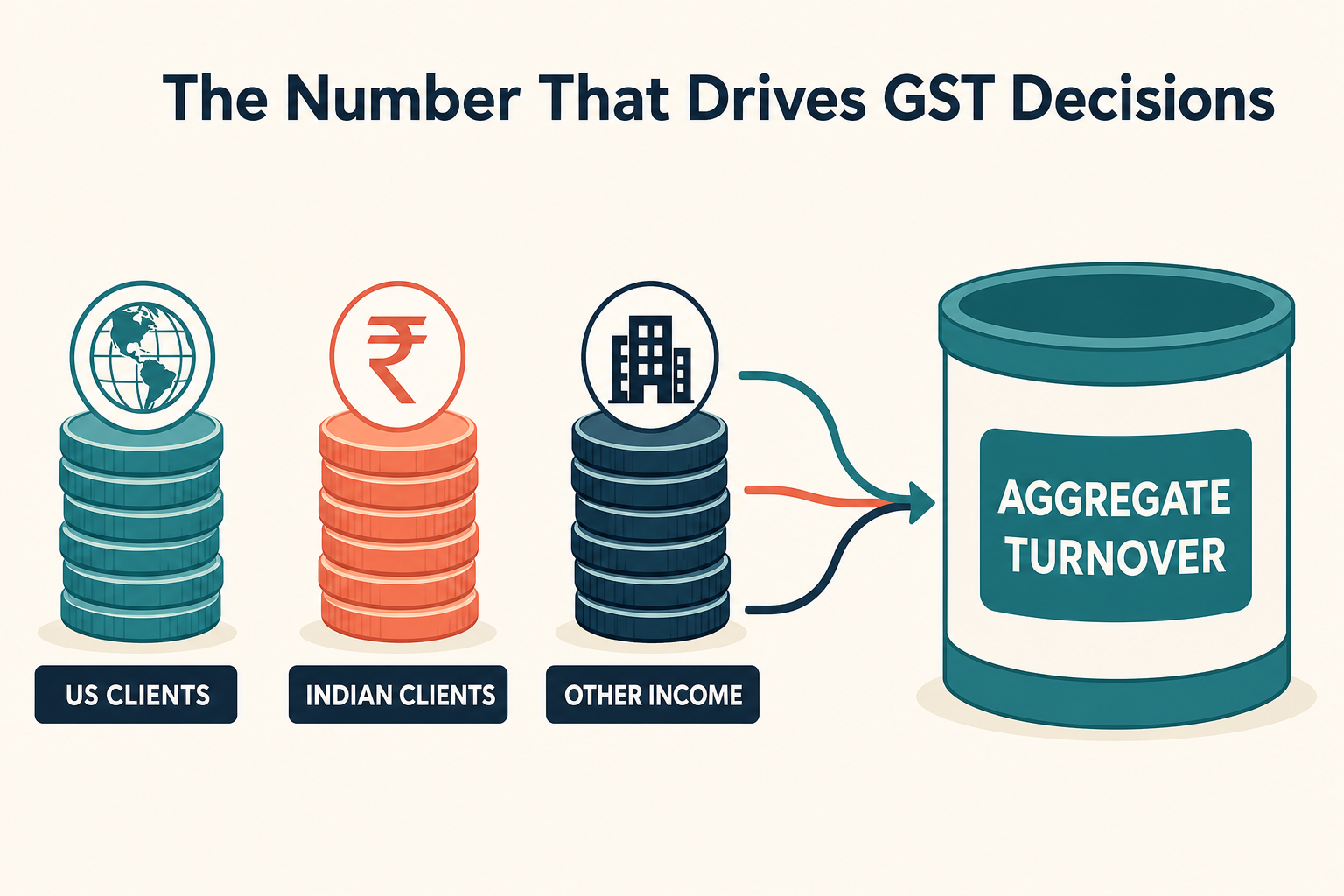

The number most freelancers should know

Aggregate turnover. Unfortunately, many freelancers underestimate it.

Common assumptions: *"I only count foreign income."* Or: *"I only count consulting revenue."* Reality can be more complicated. Depending on the facts, turnover analysis may include multiple revenue streams. This is why experienced CAs often ask broader questions than freelancers expect.

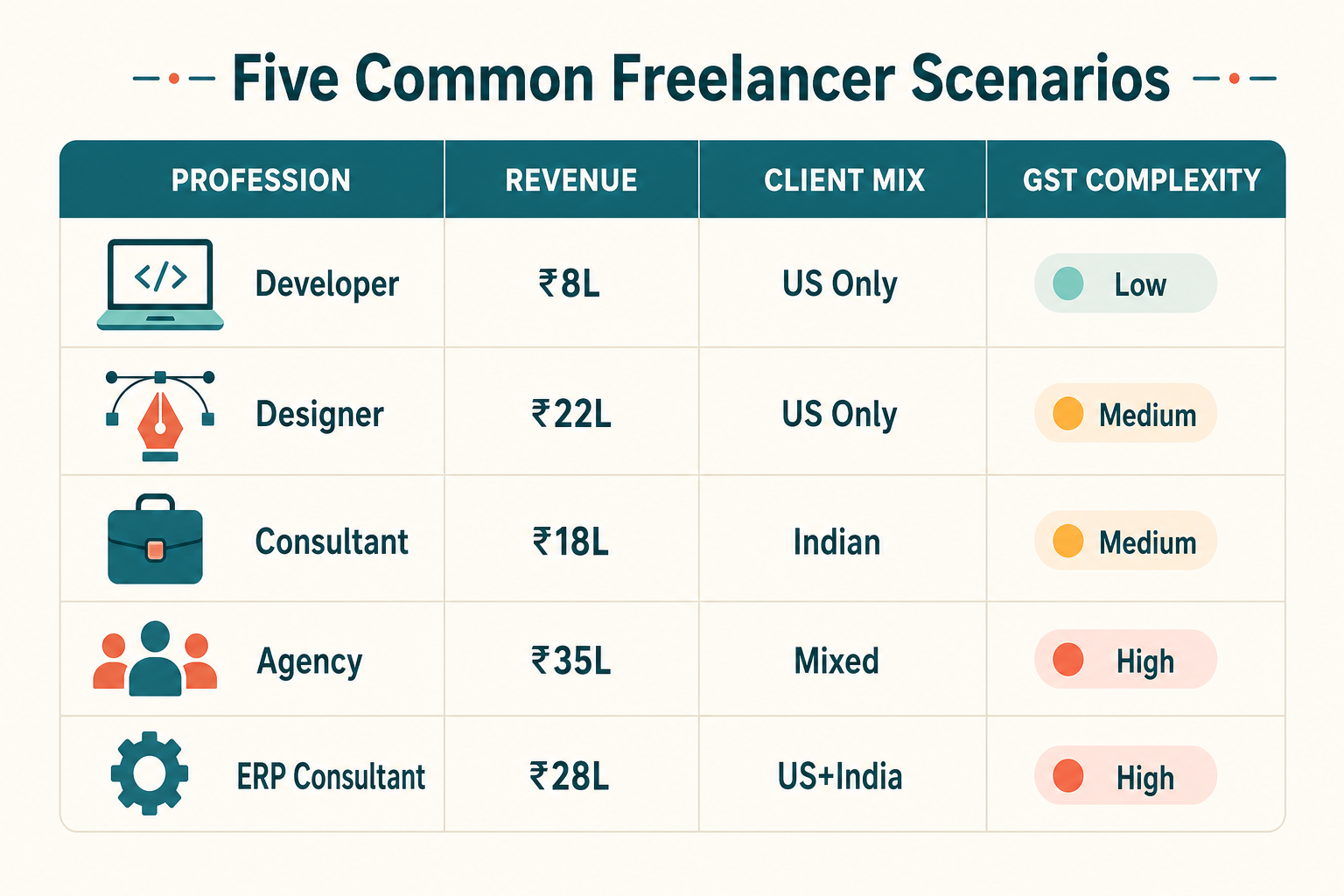

Scenario matrix

This is where things become practical. Let's examine common freelancer situations.

| Profession | Revenue | Client Mix | Initial GST Analysis |

|---|---|---|---|

| Developer | ₹8 lakh | US only | Further analysis required |

| Designer | ₹22 lakh | US only | Registration often becomes relevant |

| Consultant | ₹18 lakh | Indian clients | Different GST considerations |

| Agency owner | ₹35 lakh | Mixed clients | Registration likely becomes important |

| ERP consultant | ₹28 lakh | US + India | Requires export and domestic analysis |

The purpose of this table isn't to provide legal advice. It's to demonstrate that GST outcomes depend on facts, not labels.

The foreign client myth

One of the most persistent myths in freelancing is: *"My clients are outside India, so GST doesn't apply."*

The actual question is: *"Do these transactions qualify as exports of services under GST?"* That's a much more nuanced analysis. Export treatment depends on multiple conditions — which is why export classification deserves its own article.

📘 Stuck on whether GST registration applies to you? The Survival Guide has the full freelancer decision framework — aggregate-turnover math, foreign-client edge cases, and the registration checklist — so you stop guessing from Reddit threads.

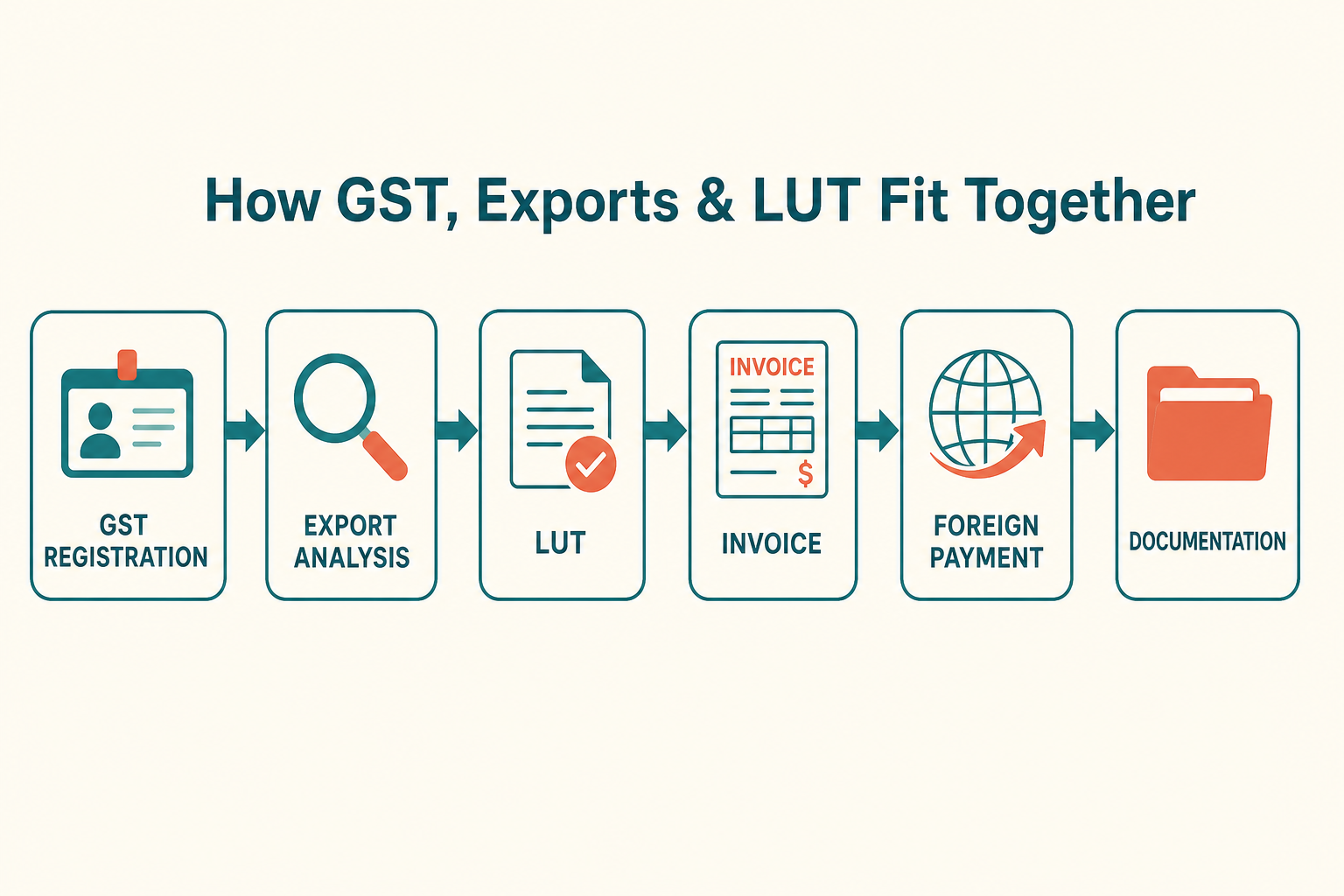

The LUT misunderstanding

Another common pattern: a freelancer discovers LUT before understanding GST registration. This creates confusion. Think of the workflow like this:

GST Registration → Export Qualification → LUT → Export Invoicing

Many freelancers try to jump directly to the last step.

Turnover examples

Let's make this more concrete.

Example 1 — NetSuite consultant. Foreign revenue ₹16 lakh, domestic ₹5 lakh, total ₹21 lakh. The consultant focuses on foreign revenue. GST analysis focuses on total turnover.

Example 2 — UI designer. Foreign ₹12 lakh, domestic ₹3 lakh, total ₹15 lakh. Very different outcome.

Example 3 — Agency owner. Foreign ₹25 lakh, domestic ₹18 lakh, total ₹43 lakh. Again, a different GST discussion entirely.

These examples demonstrate why asking *"Do freelancers need GST?"* is often the wrong question. The better question is: *"What does GST look like for my situation?"*

✅ Want a quick win first? Grab the free 5-minute GST decision checklist — we'll email the PDF and you'll know in five minutes whether GST registration applies to your situation.

Common GST registration mistakes

- Mistake #1 — Assuming foreign clients eliminate GST concerns.

- Mistake #2 — Calculating turnover incorrectly.

- Mistake #3 — Confusing GST registration with LUT.

- Mistake #4 — Ignoring export documentation.

- Mistake #5 — Taking advice from freelancers whose business looks nothing like yours.

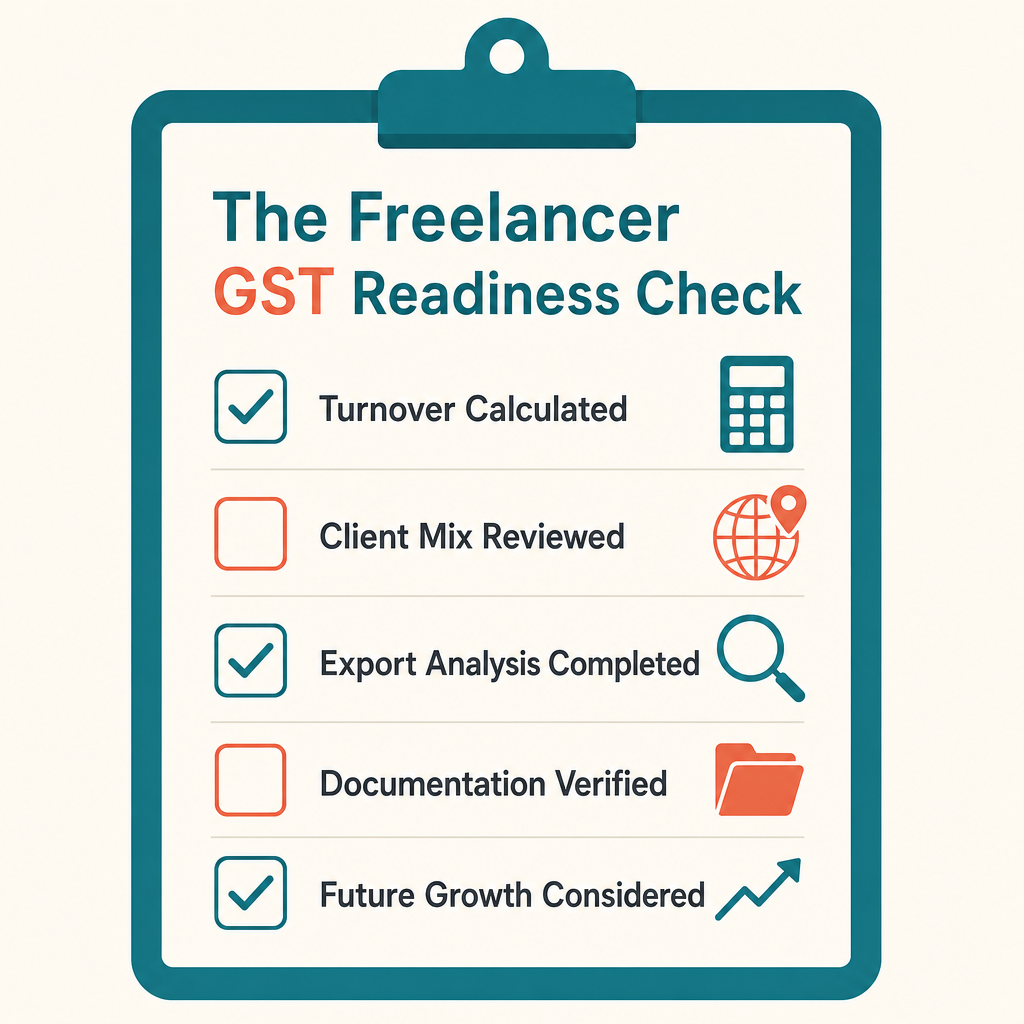

The 5-minute GST review

Whenever you're unsure, ask:

- Revenue — What is my aggregate turnover?

- Clients — Domestic, foreign, or mixed?

- Exports — Do my foreign transactions qualify as exports?

- Documentation — Am I maintaining proper records (invoices, FIRC/FIRA, contracts)?

- Growth — Will my current business model look different six months from now?

These questions often reveal more than hours spent reading random forum posts.

📖 Survival Guide Reference — Chapter 4: GST Registration Decisions. Registration decision trees, export qualification worksheets, compliance checklists, and real freelancer case studies. Get the guide →

Frequently asked questions

If all my clients are outside India, do I automatically avoid GST registration?

Not necessarily. Export analysis and registration requirements are separate questions.

Does GST registration mean I must charge 18% GST to foreign clients?

Not necessarily. Export treatment and LUT considerations may apply.

Does Wise or Payoneer affect GST registration?

Payment platforms do not determine registration requirements.

What if I have both domestic and foreign clients?

Both categories should be considered when analyzing your overall GST position.

Is LUT the same as GST registration?

No. They solve different compliance problems.

Final thoughts

Most GST mistakes happen because freelancers try to answer a complex question with a simple rule. The reality is that GST registration sits inside a larger system:

Turnover → Client Mix → Export Classification → Registration → LUT → Documentation

Once you understand that workflow, GST becomes much less intimidating. And more importantly, you stop making business decisions based on isolated pieces of advice pulled from social media.

🧭 Need this dialed in for your situation? Start with the Survival Guide for the full system, or book a 1-on-1 consultation on Topmate if you'd rather walk through your own numbers with someone.

Continue learning

Related guides on Decompiled.tax:

- The ₹20 Lakh GST Myth That Confuses Indian Freelancers

- Export of Services Under GST

- Do Indian Freelancers Charge GST to Foreign Clients?

- LUT Filing for Freelancers

- FIRC for Freelancers in India

- FIRC vs FIRA Explained

- Section 44ADA for Software Developers

For the complete GST framework covering registration, exports, LUT, FIRC/FIRA, invoicing, and documentation, see 📖 The Indian Freelancer's GST & Income Tax Survival Guide — covered across Chapters 4, 5, 7, and 8.

Want a one-on-one walkthrough of your own situation? Book a consultation on Topmate →